Compare Landis.com and Nobul.com

For Sellers

For Buyers

For Buyers

Answer: Landis.com is a rent-to-own program that does not provide real estate services while Nobul.com is a referral fee network that enables broker-to-broker collusion with use of blanket referral agreements

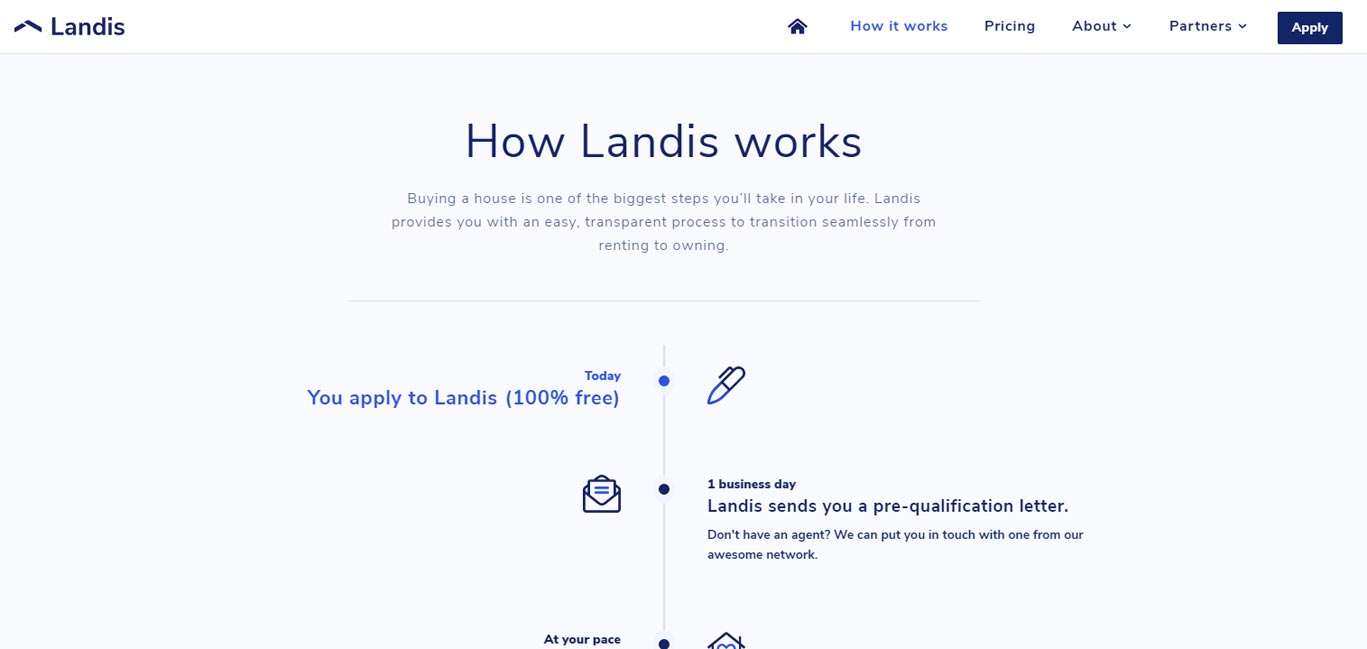

Buying with Landis

Landis is a rent-to-own program that purchases the home and then rents it out to you as a tenant. Landis claims to operate a one-year program for the tenants to buy the property once they can afford a down payment. A common complaint with all rent-to-own programs is an inability of the tenant to secure a loan in time to purchase the property, at which point the tenant is either forced to walk away with a loss or continues to rent.

Landis may sometimes suggest that a customer reach out to someone (e.g. a lender) who can help them, but the company doesn’t make money from it, and only gives the info to the customer, not the customer's info to anyone else. Landis does not receive any referral fees from third parties (such as lenders, real estate brokers, etc.) and keenly guards customers' information. This is a refreshing approach that adds value to consumers. Landis states that: "companies at our stage don't have any incentive to charge hidden fees: growth and customer experience simply matter much more than revenue."

Landis Pricing

Landis revenue comes from the price of rent and a 3% increase between the price of the home when Landis buys it and the price it sells it to the tenant after a year.

Landis is silent on what happens in a situation when the price of the home drops before the tenant can buy it, or if the mortgage rates increase during the tenancy period. When consumers use Landis, they are unable to take advantage of a buyer’s commission rebate from a real estate agent because the company is the one actually buying the home.

Landis states that it receives "no rebates or commissions from agents, we pay agents their full commission, as though they were working with the customer."

When it comes to the cost of rent Landis says that "we're very upfront with our users that during the 12 months of the program, we are more expensive than owning, or even renting. That's because we need our customers to put money to the side for their down payment … our only revenue is market rent and 3% appreciation at the end of the year. The economics work out because we're in areas where average rents are high."

Listing Services

- This Service Does Not Represent Sellers

Buyer's Agent Services

- This Service Does Not Represent Buyers

Landis.com Editor's Review:

Landis program purchases the home and rents it to the tenant with an option to buy. Landis reviews full financial, credit, and work history of each potential tenant. Those few applicants who pass the screening may select a home within the allowed amount Landis sets. A tenant pays rent, a portion of which becomes a down payment to eventually buy the home. After a year, if the tenant decides to move out, Landis deducts half of the down payment amount saved, as an added fee. When purchasing a house from Landis, a tenant must and pay closing costs of the sale.

Landis has only enough cash on hand (structured as debt) to place offers against a handful of properties. This is why the company likely rejects the majority of applications as a way to reduce risk. It is safe to assume that only a very small number of applications with Landis are approved.

According to the company, "lenders send us customers that want to buy a home but can't close on a loan. It could be due to a low credit score, insufficient down payment, a recent bankruptcy, self-employment, or some other reason."

To secure a mortgage on competitive terms is a primary and the best option to buy a home. Yes, the down payment is difficult, but adding Landis to the mix doesn't solve the overall affordability. Landis claims that owning a home is always cheaper than renting it, but Landis is a landlord.

There is nothing to substantiate that renting a home from Landis is less expensive to own it during that same time frame. There is also nothing to suggest that Landis is offering reduced rent to the tenant at any given time. Buying a property is a risk, and Landis must account for this risk with added fees. The true costs of this rent-to-buy program are incredibly difficult to estimate by anyone other than Landis, and these costs are absolutely real.

Buyers are unlikely to receive a buyer's rebate from a real estate agent when buying with Landis program.

Buying a home is one of the most important transactions in people's lives, especially the first home. By adding Landis rent-to-own proposition, buyers are subjecting their transaction to the additional 3% appreciation fees, paying rent, and a possible loss of half of the down payment amount if moving out.

Landis receives a neutral editor's score because of several factors. When asked, the company declined to disclose its application volume and applicant success rates. Lack of this information makes it difficult to estimate the “weight” of overall operations and the returns the company is required to make against the total number of participants.

An undisputed positive is that the company doesn’t make money from referrals, making their claims to hold consumers’ best interest viable.

Landis claims that owning in the long term is cheaper than renting, especially in the markets where it operates. However, there is no clear evidence money is saved and there is no evidence that consumers who choose the Landis model end up with a higher chance of purchasing the home.

Landis states: “We completely agree that a mortgage is better. That's why we coach all our customers to do what they need to get a mortgage. It's the whole point of the company. We work with those who simply can't get a mortgage (because of credit score, down payment, etc.) and we coach them to fix what prevents them from getting one. As soon as they can get one, they graduate from the program.”

We find no solid evidence that Landis offers home buyers tangible savings as part of their rent-to-own program, but at the same time, some home buyers may decide for themselves that the program is worth the added fees.

Geodoma editorial staff remains overall neutral on the subject: we can neither recommend Landis nor suggest that buyers refrain from using the program.

Where does Landis.com operate?

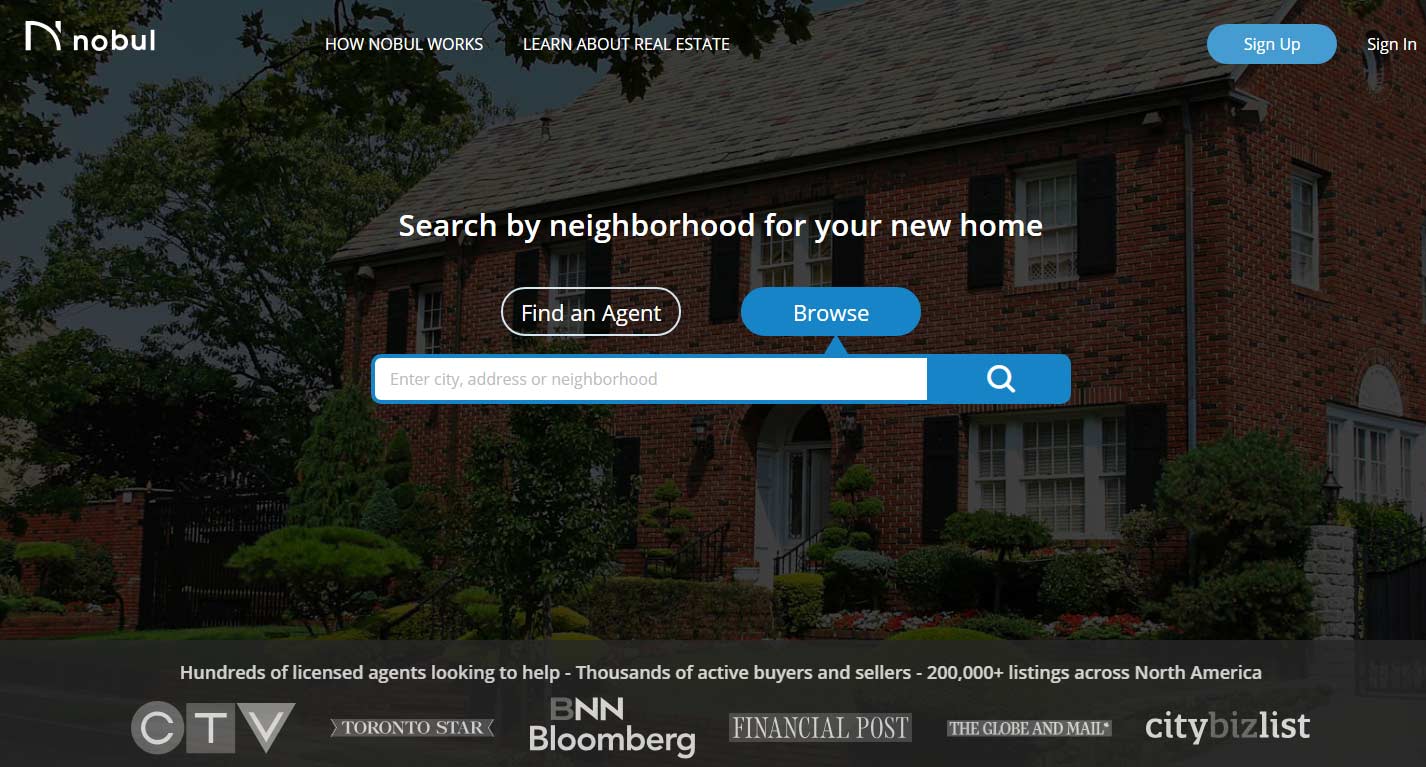

Buying and Selling with Nobul

WARNING: Unlawful Kickbacks, Broker-to-Broker Collusion, False Marketing, Wire Fraud, Price Fixing.

Nobul.com) is a broker-to-broker collusion scheme, where "partner agents" unlawfully agree to pay massive kickbacks to receive your information and engage in market allocation, consumer allocation, false advertising, unlawful kickbacks, wire fraud, and price-fixing practices in violation of, inter alia, 18 U.S.C. § 1346, 18 U.S.C. § 1343, 15 U.S.C. § 1, 15 U.S.C. § 45, 12 U.S.C. § 2607, 12 C.F.R. § 1024.14. As a consumer, you will always significantly overpay for Realtor commissions subject to hidden kickbacks and pay-to-play steering promoted in this scheme.

United States federal antitrust laws prohibit consumer allocation and blanket referral agreements between real estate companies.

Be smart; do not allow your information to be "sold as a lead" to a double-dealing Realtor in exchange for massive commission kickbacks paid from your future home sale, or your future home purchase.

Nobul works as a referral fee network that collects pricing and services data from a limited pool of Referred Agents and sends it to consumers as non-binding proposals. Nobul operates as a licensed real estate brokerage in Canada, but it does not produce any services that are typically offered by real estate agents and does not represent consumers when buying or selling real estate in any State.

Nobul is also registered as a broker in Florida under license number CQ1056639 so that it is able to collect referral fees in the United States. When consumers submit information to Nobul, this information is simply sold to real estate agents who are willing to pay for it with a share of their commission. If an Agent does not want to pay a referral fee, the consumer will not see any proposals from them using the Nobul platform.

Nobul claims to provide savings, but consumers are likely to overpay for their Referred Agent's commission due to added mandatory platform fee.

Nobul Pricing

Nobul revenue comes from referral fees and sale of user data.

Listing Services

- This Service Does Not Represent Sellers

Buyer's Agent Services

- This Service Does Not Represent Buyers

Nobul.com Editor's Review:

Nobul is a referral fee network in business to collect fees for matching brokers with consumers. Referral fees are highly disadvantageous for real estate consumers because they must be accounted for with excessive real estate commissions. Nobul Service Terms state that: “In consideration of Nobul's Referrals pursuant to this Agreement, the Agent shall pay to Nobul, a referral fee (a “Referral Fee”) based on a percentage of revenue equal to 0.2% of the purchase price of the property purchased or sold. The Agent shall pay the Referral Fee to Nobul within ten (10) days following the closing date of the purchase or sale of the property.”

One of the major expenses for real estate consumers, when buying or selling a home, is real estate service fees and closing costs associated with the purchase, or sale. Service fees and closing costs are, for the most part, a necessary expense. Real estate agents significantly help home buyers and sellers to navigate a complicated and competitive real estate process in exchange for a legitimate commission as a reward.

Other closing fees usually include required services such as property appraisals, inspections, title insurance, etc. – all in some way help to legitimize the sale and to manage risk. There can be much said with regards to managing closing costs by choosing a motivated competitive agent who is willing to offer a buyer’s refund or a competitive listing rate.

On the other hand, while claiming it saves money to consumers, Nobul simply adds referral fees into already a fee-ridden process – consumers experience false and fabricated savings in this model. In economics, this process is known as reverse competition, where consumers end up being "sold as leads" to Referred Agents.

The platform works with a limited pool of Referral Agents willing to pay a significant part of their commission to Nobul. This referral fee is back-loaded into Referred Agent's agreement, instead of being handed to the consumer directly. The consumer technically does not pay Nobul, but she ends up with a higher cost of commissions when working with their Referred Agent. Nobul is not a free platform, these fees are simply hidden inside the commission.

Let's say a real estate consumer, James, wants to hire a listing agent when selling a median-priced home for $250,000. A local competitive agent, Jill, offers James a 1.5% commission while helping him in this process. The estimated commission, in this case, is $3,750.

On the other hand, James also receives non-binding proposals using Nobul platform from Referred Agents with a referral fee attached to the back of every proposal. When James is faced with these types of proposals, results are quite different. Firmly assuming that the profit margins and service offerings remain the same for Jill and Referral Agents using Nobul, any possible buyer's refund offered by Referral Agents must be reduced to account for the Nobul referral fees.

The referral fee in this scenario estimated at $500 due to Nobul from a Referral Agent. With the profit margin fixed, the estimated commission Referral Agent may offer to James is now up by $500 set at $4,250. James just effectively paid Nobul $500 for a "service" that is supposed to be "free."

These fees significantly increase with the price of a home and damage quality of service the agent is willing to provide. One reason the amount of savings may ever be matched by Referred Agents versus Jill's competitive savings is due to broker-to-broker pricing collusion - if Referral Agent is willing to reduce their fee beyond market rates to compensate Nobul out of their own pocket, which is highly unlikely and unreasonable to assume. Because referral fees are pre-set between Nobul and Referral Agents in advance, the cost of the referral is easily incorporated with the excessive commission.

The reason we give Nobul a low score is due to exigent fees and the way these fees are structured. Nobul operates a Referral Network that commoditizes consumers as leads. With Nobul agents are forced to quote higher commissions due to added fees. The vast majority of competitive agents refuse to play this game and Nobul simply steers consumers toward a very limited pool of agents in its pay-to-play network.

As a licensed real estate agent that doesn't perform any real estate services, or takes any responsibility for the transaction, it's not entirely clear how this process works under the Business and Professions Code.

Should real estate agents distribute "bids" of other agents for a fee? If one to say that the referral fee is indeed necessary, why not structure it as an actual service fee that is properly charged, instead of having to be back-loaded into Referral Agent's agreement?

The answer is simple – if Nobul was to charge Agents for its service directly, no Agent would ever sign-up. Agents only sign-up with Nobul because the price of the referral fee can be easily incorporated into their client's agreement.

Nobul further violates the privacy of consumers because it requires Referred Agents to disclose major details about the actual home purchase or sale. Nobul states that: "The Agent shall maintain adequate records of all fees and commissions received from the Client and shall make such records available to Nobul at its request. Such records shall include copies of the applicable real estate association’s Listing Agreement, Agreement of Purchase and Sale, a statement of commission earnings and the Trade Record Sheet, as applicable."

Despite collecting the referral fee, Nobul takes absolutely no responsibility for the transaction and consumers to acknowledge and agree "that no employment, joint venture, partnership, or agency relationship exists between you and Nobul as a result of this Agreement or your use of our Services. We are solely independent contractors."

Nobul clearly doesn't provide any tangible value to the real estate consumers as a licensed real estate agent. Nobul further audits all transactions because it needs to find out how much money real estate agents receive in commissions, inevitably collecting private details of consumer’s agreement for home purchase or sale.

This effect is known as a “blind” match. Truly competitive agents who offer great savings to consumers can never use Nobul. For example, a highly competitive flat fee listing service has a set competitive price – they would never be able to pay an excessive fee amount to a third-party.

Nobul referral fee only works is with services who are silent on their commission – if a client comes directly to an agent, one price is given, if a client uses Nobul, another price is in play. We strongly believe that real estate consumers looking to buy or sell a home should always use 0% referral fee platforms in order to avoid paying a higher cost in commissions.

By using Nobul, consumers further encourage pay-to-play bias in a broken real estate industry.