Compare HomeStoryRewards.com and RamseySolutions.com (RamseyTrusted Agent)

For Sellers

For Sellers

For Buyers

For Buyers

Answer: Both HomeStoryRewards.com and RamseySolutions.com (RamseyTrusted Agent) function as a referral fee network that enables broker-to-broker collusion with use of blanket referral agreements.

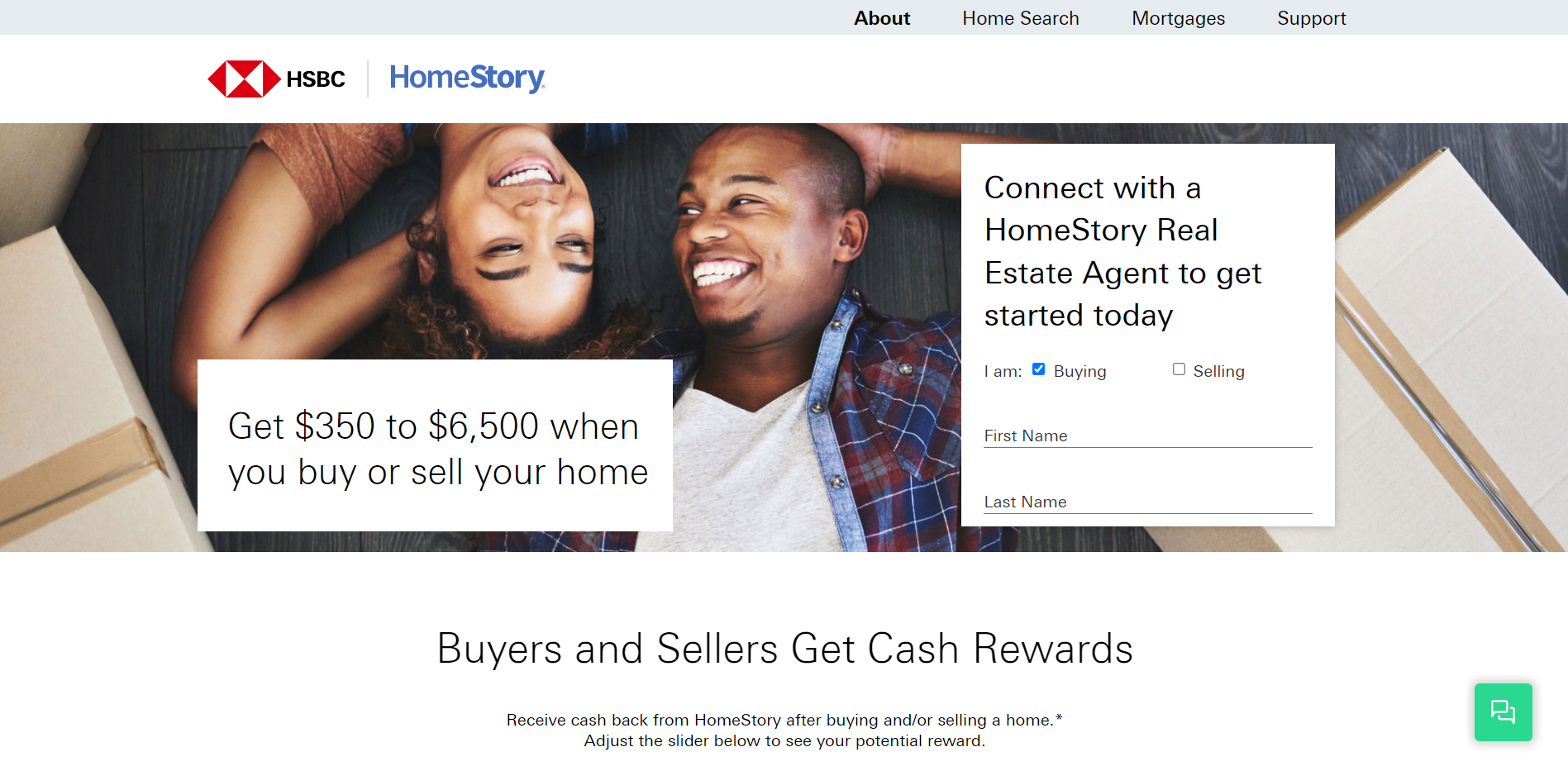

Buying and Selling with HomeStory

WARNING: Unlawful Kickbacks, Broker-to-Broker Collusion, False Marketing, Wire Fraud, Price Fixing.

HomeStoryRewards.com) is a broker-to-broker collusion scheme, where "partner agents" unlawfully agree to pay massive kickbacks to receive your information and engage in market allocation, consumer allocation, false advertising, unlawful kickbacks, wire fraud, and price-fixing practices in violation of, inter alia, 18 U.S.C. § 1346, 18 U.S.C. § 1343, 15 U.S.C. § 1, 15 U.S.C. § 45, 12 U.S.C. § 2607, 12 C.F.R. § 1024.14. As a consumer, you will always significantly overpay for Realtor commissions subject to hidden kickbacks and pay-to-play steering promoted in this scheme.

United States federal antitrust laws prohibit consumer allocation and blanket referral agreements between real estate companies.

Be smart; do not allow your information to be "sold as a lead" to a double-dealing Realtor in exchange for massive commission kickbacks paid from your future home sale, or your future home purchase.

HomeStory is a price-fixing scheme that allocates home buyers to colluding Realtors through a "shell" real estate entity. When consumers submit information on the HomeStory website, this information is simply shared in exchange for an undisclosed fee with real estate agents in a process known as a pay-to-play steering and a "blind match." HomeStory Real Estate Services, Inc. "shell" entity colludes and price-fixes commissions with various Realtors affiliated with Keller Williams, Weichert, Christie's, RE/MAX, ERA, Compass, Coldwell Banker, Better Homes & Gardens, Berkshire Hathaway, eXp Realty, Exit, Fathom, Sotheby's, Century 21, HomeSmart, and others.

HomeStory Pricing

HomeStory fees come from hidden kickbacks, set at 25% to 40% of the gross commission received by a network of colluding Realtors.

Listing Services

- This Service Does Not Represent Sellers

Buyer's Agent Services

- This Service Does Not Represent Buyers

HomeStoryRewards.com Editor's Review:

HomeStory Real Estate Services, Inc. (dba HomeStory, HomeStory.com, HomeStoryRewards, HomeStoryRewards.com) is a licensed real estate entity in the State of Texas License No. 605602 operates as a "shell" broker to collect an undisclosed referral fee, set at 25% to 40% from the gross commissions paid by all colluding Realtors in the network. This fee is inevitably passed down to consumers in a form of inflated real estate commissions when selling a home.

More importantly, HomeStory is a licensed real estate entity that does not engage in actual real estate broker services. HomeStory systematically applies pay-to-play bias towards all Realtor matching results, meaning, only Realtors that have agreed to collude and pay a referral fee are matched with consumers.

Realtors only sign-up with HomeStory because the price of the referral fee can be easily incorporated into their client's agreement with excessive commissions.

HomeStory receives a low Editor's rating because this service is a biased hub-and-spoke broker-to-broker collusion scam, that falsely claims to provide an independent and unbiased service of matching consumers with agents.

HomeStory operates on a pay-to-play methodology to collect junk fees that needlessly make home buying and selling more expensive. In this scheme, consumers are no longer in the driver's seat, but instead, are traded as a commodity between brokers.

HomeStory plays junk fees down, claiming there are "no upfront costs" to Realtors and the service is "free" and "no obligation" to consumers, but it rigidly locks every participating Realtor into a kickback attached to the back-end of every agreement that restrains free trade. As a licensed real estate entity that doesn’t perform any real estate services or take any responsibility for the transaction, this scheme operates to unlawfully allocate consumers and bypass RESPA anti-kickback regulations through a "shell" entity.

Consumer brokering is an act of selling information of potential home buyers and home sellers (paid referrals) between real estate brokers, in exchange for a cut of a broker’s commission. Brokers on each side of the adopted scheme, cause direct damage to the real estate representation market with reverse competition, anticompetitive market allocation, price-fixing, lack of competition, limited choices to consumers, unnecessary high commissions, and improperly negotiated fees. A referring broker in this scheme does not compete with referred brokers, instead, HomeStory administers a series of agreements that restrain free trade, disguised as Realtor matching services.

12 C.F.R. § 1024.14(g)(1)(v) (Regulation X) and RESPA 12 U.S.C. § 2607(c)(3) narrowly allow payments pursuant to cooperative brokerage and referral arrangements between real estate agents and real estate brokers. This limited exemption on kickbacks only applies to fee divisions within real estate brokerage arrangements when all parties are acting in a real estate brokerage capacity. HomeStory does not act in a brokerage capacity, in fact, this entity willfully chooses to disengage from offering real estate representation services to consumers, as the core premise to create successful collusion through interstate wire communication to further the scheme. Wire fraud is financial fraud involving the use of any telecommunications or information technology.

Real estate transaction is a rare, high-value, and high-risk-aversion experience that is easily subjected to unlawful kickbacks, especially with the use of the Internet. Consumers are often subjected to high commissions and hidden referral fees without a full understanding that these fees increase their commissions and result in a lower quality of service. Whenever any double-dealing Realtor agrees to pay these massive kickbacks, he or she is unable to offer full and competitive representation services to anyone. HomeStory does not cater to honest Realtors, it only caters to Realtors willing to cheat their clients out of full services, and willing to share private information about their clients' transactions with the scheme.

HomeStory antitrust and consumer protection violations are not harmless. Realtors who attempt to compete for consumers on fair terms and competitive pricing are at a massive disadvantage in this environment. As a result of broker-to-broker collusion, consumers end up getting steered toward a limited pool of agents and overpay for commissions. Consumers’ private transaction information is always shared with a referring broker that requires it to be disclosed to calculate the referral fees to be paid at the close of each transaction.

Consumers, of course, pay for this abuse with higher costs of commissions that, eventually, make it directly into their new mortgages and cause significant losses of net equity from a home sale.

HomeStory utilizes several high-profile financial institutions and lending channels to promote price-fixing and fraud to consumers across state borders, such as HSBC Bank USA, JPMorgan Chase Bank NA, Lakeview Loan Servicing, LLC, The Money Source Inc., Alliant Credit Union, Home Point Financial, etc.

| HOME VALUE | REWARD |

| $0 - $99K | $350 |

| $100K - $149K | $650 |

| $150K - $249K | $900 |

| $250K - $349K | $1,000 |

| $350K - $449K | $1,250 |

| $450K - $499K | $1,750 |

| $500K - $549K | $2,000 |

| $550K - $599K | $2,300 |

| $600K - $699K | $2,400 |

| $700K - $799K | $2,750 |

| $800K - $899K | $3,100 |

| $900K - $999K | $3,500 |

| $1.0M - $1.099M | $4,000 |

| $1.1M - $1.199M | $4,350 |

| $1.2M - $1.299M | $4,750 |

| $1.3M - $1.399M | $5,500 |

| $1.4M - $1.499M | $6,000 |

| $1.5M+ | $6,500 |

Obviously, these are plain price fixed amounts imposed by HomeStory on random brokerages. All of this is done to profit from the largest number of transactions, without actually performing the service of a real estate broker. The scheme is disguised as if consumers are saving money, but in reality, consumers lose money in hidden kickbacks.

For example, on a home purchase of $1 million, Home Story price-fixes the rebate for ALL "partner agents" at $4,000. What the scheme fails to mention is that the kickback HomeStory secretly takes (assuming a 30% kickback) from that same transaction is $9,000 - more than double the amount the consumer receives. On the open market, consumers can easily receive a buyer rebate valued at $15,000 or more, instead of a price-fixed $4,000 amount. This $9,000 loss is, obviously, the price difference between wire fraud, false advertising, collusion, price-fixing, as opposed to open competition. Moreover, honest agents able to offer even better terms to consumers on the open market are bypassed by this scheme entirely. Price fixing does not only harm consumers, but it harms all honest participants outside of the scheme, as well as the open nature of the real estate market itself.

HomeStory shell broker does not connect consumers with anyone outside the network, in fact, they specifically steer consumers into the network in exchange for massive kickbacks pre-negotiated in advance.

There are numerous reasons why consumers are wise to avoid the HomeStory scheme, but probably the most important reason is that the lack of transparency and honesty is contagious. HomeStory scheme attracts ONLY double-dealing Realtors who are willing to break a host of federal antitrust laws, and unwilling to compete for consumers with transparency. An unethical Realtor will always find a way to turn the most important transaction into a self-dealing proposition - to collect a bigger commission check faster without any regard for what is truly a good deal for their clients.

Why Does HomeStory Engage in Price-Fixing?

HomeStory engages in price-fixing because it needs a "dangling carrot in front of consumers" to "reasonably" justify the kickbacks it takes from the Realtors who patriciate in the scheme. This dynamic is better known as a hub-and-spoke conspiracy. In a hub-and-spoke type conspiracy, all listing rates are set at the same amount for all Realtors, where none of the "partner agents" compete with one another on pricing at all. HomeStory scheme produces absolutely no tangible service as a licensed broker to anyone and instead delivers inflated prices and lower quality of service. The scheme originates as a conspiracy to restrain trade and to funnel consumers toward the scheme and away from the open market. There are hundreds of thousands of highly competitive Realtors who offer great savings and great service, and they refuse to pay kickbacks or to comply with the price fixed rates set by HomeStory.

The illicit 25% kickback is the reason why HomeStory setsHSBC HomeStory listing commission rates for Realtors outside their firm. ALL consumers and ALL legitimate Realtors are scammed by HomeStory, even if the experience and savings may seem "good enough" because price-fixing is a faulty shortcut to genuine open competition between Realtors. By law, all Realtors must compete for consumers and set prices individually. Open competition is at the core of our free and independent society everywhere in America.

The Realtor commissions in the United States have long suffered from the "standard" 6% myth and the false notion that "buyer agents work for free." However, these myths cannot be resolved with price-fixing of commissions to some other level, in exchange for kickbacks. ALL Realtors who participate in the HomeStory scheme are engaged in price-fixing. The Sherman Act imposes criminal penalties of up to $100 million for a corporation and $1 million for an individual, along with up to 10 years in prison for each count. Persons found guilty of wire fraud under federal law face fines up to $250,000 for individuals and up to $500,000 for organizations, subject to imprisonment of not more than 20 years. There are additional penalties of 30 years imprisonment and a million-dollar fine if the wire fraud involves a financial institution. These penalties are per count, which means that each electronic communication can be considered as a separate count. No legitimate Realtor will ever willingly allow themselves to be exposed to such massive liability.

The best, highly-experienced, well-educated, law-abiding, honest, and ethical Realtors will never participate in price-fixing because it is a felony that carries massive penalties. The best Realtors can recognize price-fixing as wrong because they respect the true value of honest negotiations.

The prices set by HomeStory are not for the services that they offer, but for services offered by their direct competitors – other brokers. When HomeStory refuses to compete with these brokers and instead organizes "partner agents" into a network, it breaks an entire host of basic principles that guide our open and fair markets. Moreover, HomeStory extends this conspiracy all across the United States, making the scheme highly damaging due to the scaled use of the Internet to transmit collusion. The Internet, like any other scaled information medium, can be used to transmit open competition just as easily as pay-to-play fraud and collusion.

HomeStory wire fraud scheme is particularly alarming because it is scaled across state borders by financial institutions such as HSBC Bank USA, JPMorgan Chase Bank NA, Lakeview Loan Servicing, LLC, The Money Source Inc., Alliant Credit Union, Home Point Financial, etc. in an open violation of RESPA and Sherman Antitrust Act by means of wire communications interstate channels such as the following:

HSBC HomeStory wire fraud channel

Fidelity HomeStory wire fraud channel

Chase Homestory wire fraud channel

The short answer is: HomeStory's intent to fix prices is directly tied into the kickbacks it receives from the "partner agents." This dynamic is a product of the restraint of genuine competition. The "standard commissions" problem in the residential real estate sector can only be fixed legally by encouraging Realtors to set and advertise competitive prices to consumers at scale without paying any kickbacks.

Where does HomeStoryRewards.com operate?

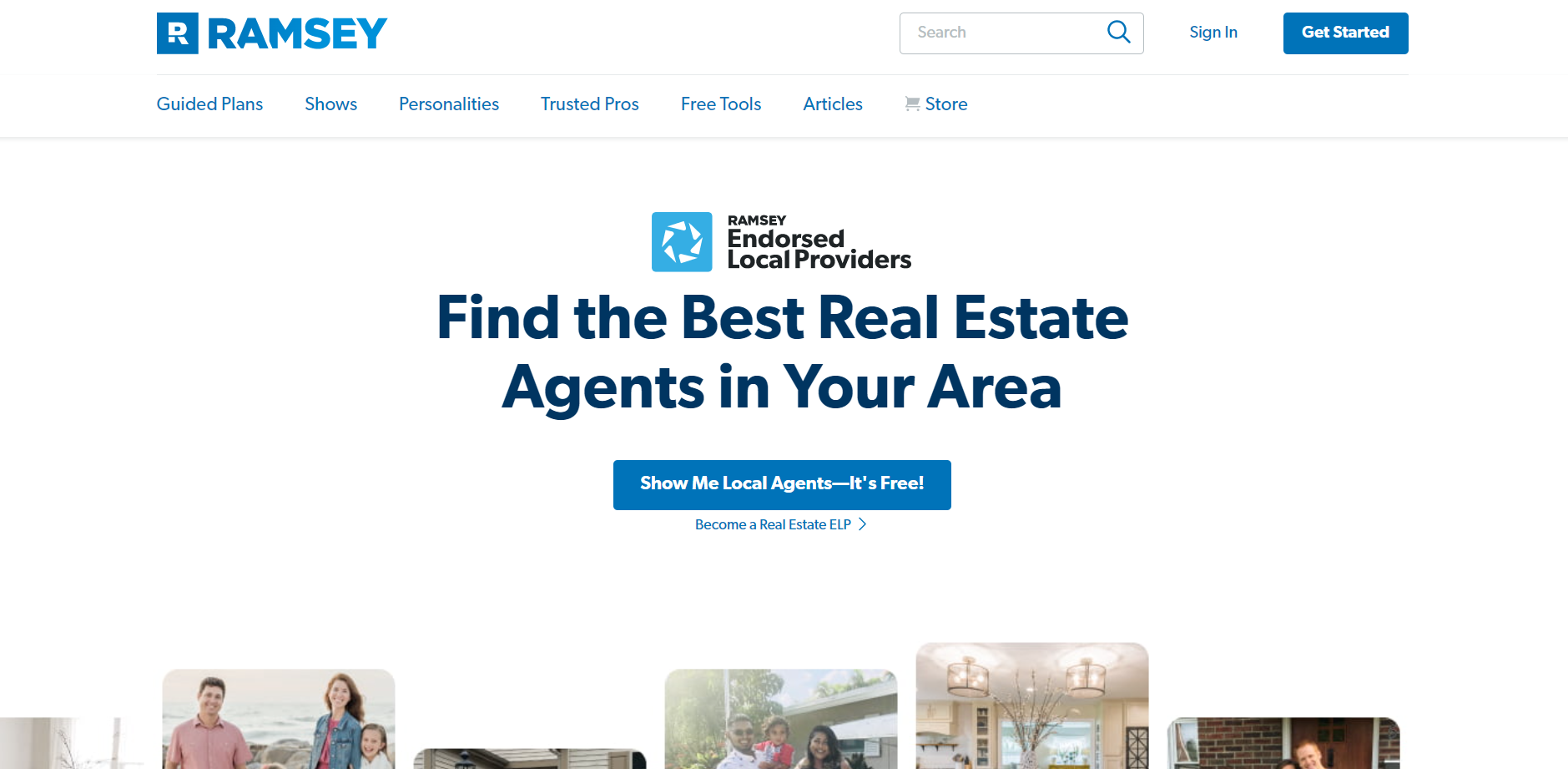

Buying and Selling with Ramsey ELP

WARNING: Unlawful Kickbacks, Broker-to-Broker Collusion, False Marketing, Wire Fraud, Price Fixing.

RamseySolutions.com (RamseyTrusted Agent)) is a broker-to-broker collusion scheme, where "partner agents" unlawfully agree to pay massive kickbacks to receive your information and engage in market allocation, consumer allocation, false advertising, unlawful kickbacks, wire fraud, and price-fixing practices in violation of, inter alia, 18 U.S.C. § 1346, 18 U.S.C. § 1343, 15 U.S.C. § 1, 15 U.S.C. § 45, 12 U.S.C. § 2607, 12 C.F.R. § 1024.14. As a consumer, you will always significantly overpay for Realtor commissions subject to hidden kickbacks and pay-to-play steering promoted in this scheme.

United States federal antitrust laws prohibit consumer allocation and blanket referral agreements between real estate companies.

Be smart; do not allow your information to be "sold as a lead" to a double-dealing Realtor in exchange for massive commission kickbacks paid from your future home sale, or your future home purchase.

Ramsey ELP is a broker-to-broker collusion scheme that allocates home buyers and home sellers to colluding Realtors through a "shell" real estate entity. When consumers submit information on the Ramsey Solutions website, this information is sold in exchange for an undisclosed fee with real estate agents in a process known as a pay-to-play steering and a "blind match." Ramsey Solutions (dba The Lampo Group, LLC) is a Tennessee Real Estate Firm "shell" that openly allocates consumers with various Realtors affiliated with Keller Williams, RE/MAX, Coldwell Banker, Better Homes & Gardens, Berkshire Hathaway, Century 21, HomeSmart, and others.

Ramsey ELP Pricing

Ramsey ELP fees come from hidden kickbacks, set at 30% of the gross commission received by a network of colluding Realtors. Realtors also pay some up-front fees to be listed.

Listing Services

- This Service Does Not Represent Sellers

Buyer's Agent Services

- This Service Does Not Represent Buyers

RamseySolutions.com (RamseyTrusted Agent) Editor's Review:

The Lampo Group, LLC (dba Ramsey Solutions) is a licensed real estate firm in the State of Tennessee License No. 221042 operates as a "shell" broker to collect an undisclosed referral fee, set at 30% from the gross commissions, paid by all colluding Realtors in the Ramsey Endorsed Local Provider (ELP) network. This fee is inevitably passed down to consumers in a form of inflated real estate commissions when selling or buying any home.

More importantly, Ramsey ELP is an active licensed real estate entity that does not engage in actual real estate broker services. Ramsey ELP systematically applies pay-to-play bias towards all Realtor matching results, meaning, only Realtors that have agreed to collude and pay a referral fee are matched with consumers.

Realtors only sign-up with Ramsey ELP because the price of the referral fee can be easily incorporated into their client's agreement with excessive commissions.

Ramsey ELP receives a low Editor's rating because this service is a biased hub-and-spoke broker-to-broker collusion scam, that falsely claims to provide an independent and unbiased service of matching consumers with agents.

Ramsey ELP operates on a pay-to-play methodology to collect junk fees that needlessly make home buying and selling more expensive. In this scheme, consumers are no longer in the driver's seat, but instead, are traded as a commodity between licesned brokers.

Ramsey ELP plays junk fees down, claiming that the service is "free" and "no obligation" to consumers, but it rigidly locks every participating Realtor into a kickback attached to the back-end of every agreement that restrains free trade. As a licensed real estate entity that doesn’t perform any real estate services or take any responsibility for the transaction, this scheme operates to unlawfully allocate consumers and bypass RESPA anti-kickback regulations through a "shell" entity. Ramsey ELP scam operates on a false notion that all buyer agent and listing agents commissions are the same, where no Realtor in the Ramsey ELP scheme competes for consumers on pricing.

Consumer brokering is an act of selling information of potential home buyers and home sellers (paid referrals) between real estate brokers, in exchange for a cut of a broker’s commission. Brokers on each side of the adopted scheme, cause direct damage to the real estate representation market with reverse competition, anticompetitive market allocation, price-fixing, lack of competition, limited choices to consumers, unnecessary high commissions, and improperly negotiated fees. A referring broker in this scheme does not compete with referred brokers, instead, Ramsey ELP administers a series of agreements that restrain free trade, disguised as Realtor matching services.

12 C.F.R. § 1024.14(g)(1)(v) (Regulation X) and RESPA 12 U.S.C. § 2607(c)(3) narrowly allow payments pursuant to cooperative brokerage and referral arrangements between real estate agents and real estate brokers. This limited exemption on kickbacks only applies to fee divisions within real estate brokerage arrangements when all parties are acting in a real estate brokerage capacity. Ramsey ELP shell entity does not act in a brokerage capacity, in fact, this entity willfully chooses to disengage from offering real estate representation services to consumers, as the core premise to create successful collusion through interstate wire communication to further the scheme. Wire fraud is financial fraud involving the use of any telecommunications or information technology.

Real estate transaction is a rare, high-value, and high-risk-aversion experience that is easily subjected to unlawful kickbacks, especially with the use of the Internet. Consumers are often subjected to high commissions and hidden referral fees without a full understanding that these fees increase their commissions and result in a lower quality of service. Whenever any double-dealing Realtor agrees to pay these massive kickbacks, he or she is unable to offer full and competitive representation services to anyone. Ramsey ELP does not cater to honest Realtors, it only caters to Realtors willing to cheat their clients out of full services, and willing to share private information about their clients' transactions with the scheme.

Ramsey ELP antitrust and consumer protection violations are not harmless. Realtors who attempt to compete for consumers on fair terms and competitive pricing are at a massive disadvantage in this environment. As a result of broker-to-broker collusion, consumers end up getting steered toward a limited pool of agents and overpay for commissions. Consumers’ private transaction information is always shared with a referring broker that requires it to be disclosed to calculate the referral fees to be paid at the close of each transaction.

Consumers, of course, pay for this abuse with higher costs of commissions that, eventually, make it directly into their new mortgages and cause significant losses of net equity from a home sale.

A typical broker-to-broker collusion scheme often attempts to fool consumers with heavily advertised campaigns on Google, Nextdoor, Facebook, or local radio and TV. Such a false ad might read: "Unbiased. Get Data-Driven Results. Our Agents Can Get You the Best Deals. Sign Up Now! Save Time & Hassle and Get Matched to the Perfect Agent for Your Needs. Find Quality Realtors. Top Agent Rankings. Personalized & Fast. 100% Free. Top 1% of Real Estate Agents Compete to Sell Your Home. No Obligation. Save Thousands."

In reality, all such "matches" are 100% biased, pay-to-play collusion steering mechanisms between licensed brokers, and they all cost consumers tens of thousands compared to open market savings. These "paper" brokers do not connect consumers with anyone outside the network, in fact, they specifically steer consumers into the network in exchange for massive kickbacks pre-negotiated in advance.

There are numerous reasons why consumers are wise to avoid the Ramsey ELP scheme, but probably the most important reason is that the lack of transparency and honesty is contagious. Ramsey ELP scheme attracts ONLY double-dealing Realtors who are willing to break a host of federal antitrust laws, and unwilling to compete for consumers with transparency. An unethical Realtor will always find a way to turn the most important transaction into a self-dealing proposition - to collect a bigger commission check faster without any regard for what is truly a good deal for their clients.

Why Does Ramsey ELP Engage in Collusion?

Ramsey ELP engages in consumer allocation because it is an active real estate entity that refuses to compete with other real estate agents who patriciate in the scheme. This dynamic is better known as a hub-and-spoke conspiracy. In a hub-and-spoke type conspiracy, all listing rates are set at the same amount for all Realtors, where none of the "partner agents" compete with one another on pricing at all. Ramsey ELP scheme produces absolutely no tangible service as a licensed broker to anyone and instead delivers inflated prices and lower quality of service. The scheme originates as a conspiracy to restrain trade and to funnel consumers toward the scheme and away from the open market. There are hundreds of thousands of highly competitive Realtors who offer great savings and great service, and they refuse to pay kickbacks or collude with Ramsey ELP.

The illicit 30% kickback is the reason why Ramsey ELP colludes with Realtors outside their firm. ALL consumers and ALL legitimate Realtors are scammed by Ramsey ELP, even if the experience may seem "good enough" because collusion is a faulty shortcut to genuine open competition between Realtors. Federal laws require all Realtors to compete for consumers and to deliver a tangible service, a simple test The Lampo Group, LLC real estate firm decisively fails. Open competition is at the core of our free and independent society everywhere in America.

The Realtor commissions in the United States have long suffered from the "standard" 6% myth and the false notion that "buyer agents work for free." ALL Realtors who participate in the Ramsey ELP scheme are engaged in plain collusion, where each Realtor knows that Ramsey shell brokerage will not compete at all, in exchange for a blanket kickback from the home sale or a home purchase. The Sherman Act imposes criminal penalties of up to $100 million for a corporation and $1 million for an individual, along with up to 10 years in prison for each count. Persons found guilty of wire fraud under federal law face fines up to $250,000 for individuals and up to $500,000 for organizations, subject to imprisonment of not more than 20 years. There are additional penalties of 30 years imprisonment and a million-dollar fine if the wire fraud involves a financial institution. These penalties are per count, which means that each electronic communication can be considered as a separate count. No legitimate Realtor will ever willingly allow themselves to be exposed to such massive liability.

The best, highly-experienced, well-educated, law-abiding, honest, and ethical Realtors will never participate in collusion because it is a felony that carries massive penalties. The best Realtors can recognize collusion as wrong because they respect the true value of honest negotiations.

When Ramsey ELP refuses to compete with these brokers and instead organizes "partner agents" into a network, it breaks an entire host of basic open commerce principles that guide our open and fair markets. Moreover, Ramsey ELP extends this conspiracy all across the United States via its website, making the scheme highly damaging due to the scaled use of the Internet to transmit collusion. The Internet, like any other scaled information medium, can be used to transmit open competition just as easily as pay-to-play fraud.

Most consumers do not know that Ramsey Solutions (dba The Lampo Group, LLC) is a Tennessee Real Estate Firm because the nature of the scam requires this information to be deliberately hidden. The short answer is: Ramsey ELP's intent to allocate consumers as a secret real estate shell entity is directly tied into the kickbacks it receives from the "partner agents." This dynamic is a product of the restraint of genuine competition. The "standard commissions" problem in the residential real estate sector can only be fixed legally by encouraging Realtors to set and advertise competitive prices to consumers at scale without paying any kickbacks.